26

infrastructure

investor

may

2014

pressure to do deals,” says a fundmanager.

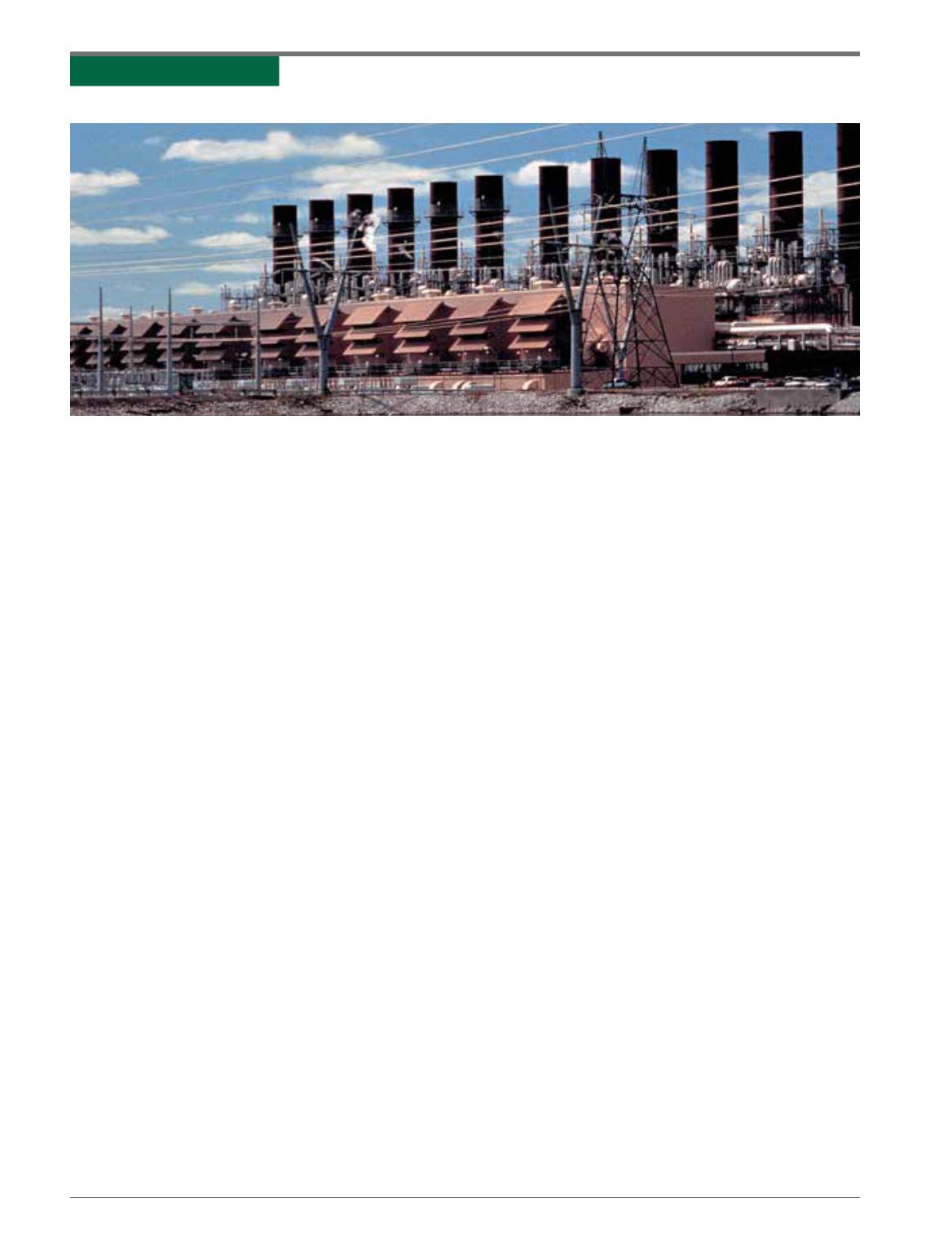

The platform sealed its first transac-

tion last July when buying a one-third

stake in Midland Cogeneration Venture

(MCV), a US combined-cycle gas-fired

power plant. Yet few would describe

this maiden transaction, reported to be

worth about $1 billion, as an adventur-

ous move: GSIA acquired its share of the

plant from Borealis, which had bought

the asset inDecember 2012. OMERS kept

the remaining two-thirds on its books.

Observers doubt deals will line up

more rapidly in the near future – partly

because they think Borealis’ deal sourc-

ingmethods are inconsistent withGSIA’s

stated strategy. “They’re promising to

create an environment where there’s

not a lot of competition and yet the first

places they go to are places where there

is a lot of competition,” says a top invest-

ment bank executive.

As an example he cites Borealis’ bid

for UK water business Severn Trent last

year – which he describes as “a hostile

bid for one of three remaining publicly

listed waste water companies, immedi-

ately before the beginning of a regula-

tory process, at 1.3 times the company’s

closing price.” The bid was later rejected

by Severn Trent, and Borealis dropped

plans to buy the asset.

The bank executive points to Borealis’

investment in Fortum’s Finnish grid last

December – and its reported interest in

Australian toll road operator Queens-

land Motorways – as further evidence

that the firm remains largely focused on

auction processes. “We’ve yet to see an

announcement of a deal which they’ve

sourced using their network and where

there’s very low competition.”

ALWAYS A BIGGER FISH

Some others dispute the soundness of

GSIA’s investment thesis. “It would be a

simple world if as soon as you get above

$5 billion there’s only one bidder. You typi-

cally see some formof competition around

everything,” says the investment banker.

Transactions of that size, argue indus-

try insiders, remain “perfectly accessible”

for investors coming together as part of

consortia: German gas transmission busi-

ness OpenGrid Europe, for example, was

acquired by aMacquarie-led consortium

in 2012 for €3.2 billion.

Bidders also have to consider the

growing firepower of general partners

(GPs), which are now capable of writing

substantial cheques from their own fund

or together with co-investors. Participants

in large auctions, while fewer than in pro-

cesses involving smaller assets, tend to be

“much more sophisticated,” says a senior

industry participant.

Others underline the fierce com-

petition foreign bidders face in core

infrastructure markets, where locals are

seen as “very competitive” with “a very

low cost of capital”.

It probably doesn’t help, observers

point out, that only two or three such

assets are put on the market every year.

Indeed, a source familiar with the

platform says it has a typical “five years or

so” investment period. Deploying more

than $12 billion in assets, worth around

$2 billion each, will thus require the vehi-

cle to close at least one or two deals a

year. Simple maths makes it easy to see

why, failing proprietary deals, achieving

this will be no easy feat.

“If only a couple of those assets are

popping up a year you are under a lot

of pressure to deploy into those deals –

which then undermines your leverage

with the vendor because the vendor

knows that too.”

NOT SO NIMBLE

Another potential Achilles heel, says a

fund manager, lies in the looseness of

the platform’s structure.

“If you want to move real time in the

process, you want to be seen to be agile

and able to play where others can’t. It’s

pretty challenging if you don’t really

know whether the capital’s there with

you for sure. That undermines your

credibility with the vendor and makes

you less nimble.”

SPECIAL FEATURE

MCV

: maiden deal