53

may

2014

infrastructure

investor

SPECIAL FEATURE

exposure simultaneously, there is likely to

be volatility in share prices for a prolonged

period and there is very little action that

companies will be able to take. What they

can do is continue to educate investors in

advance about their valuations and likely

future performance characteristics in dif-

ferent economic environments.

SUPPLY OF INVESTMENT

OPPORTUNITIES

Secondary investing inPPP/PFI infrastruc-

ture was, until recently, largely the preserve

of specialist fund managers, well versed in

the sector’s development and contractual

nuances. The listed investment companies

had been able to take advantage of their

manager’s expertise to source investments.

Typically the sellers of these investments

were a mixture of banks selling non-core

assets, construction companies recycling

capital for new investments and primary

infrastructure investors taking profits after

the completion of construction.

Over the past few years, there has been

a consistent supply of assets fromthird-party

sellers to the listed infrastructure compa-

nies, especially minority stakes in projects

they already owned. The nature of the

dynamics of the market has enabled the

buyers of secondary PPP/PFI assets tomain-

tainpricing discipline while also deploying

the capital raised in the listed market.

The supply and demand market

dynamic for secondary PPP/PFI project

assets has, however, changed significantly

over the past year or so. The strong returns

and the more established track record of

the asset class have attracted more capital

to the space, largely from institutions (pen-

sion funds and insurancecompanies), which,

directly or indirectly, have invested through

the launchof newprivate investment funds.

The increasedcompetition for assets has put

pressure on pricing, especially where port-

folio sales are conducted through auctions.

At the same time, the supply of assets

from the most motivated sellers (those

with pressure on their balance sheets post-

financial crisis) has been gradually worked

through and the slowdown innewPPP/PFI

deals being closedhas started to impact on

operational project deal flow in the second-

ary market. Recent commentary and anec-

dotal evidence suggests that pricing, espe-

cially in theUK, has increased considerably.

While this is positive for current valuations,

it is provinghard for investment companies

to make non-dilutive acquisitions.

The lack of transparency on the pric-

ing of new transactions, not just limited to

the discount rate but the conservativeness

(or otherwise) of the assumptions on cash

flows, means that it is hard for investors

in the listed companies to judge whether

acquisitions are in their continued interests.

Independent boards of directors need to

ensure that companies do not grow for the

sake of assets undermanagement (and the

additional fees paid to the investmentman-

ager) at the cost of future performance.

The other risk is that companies

broaden their investment remits to main-

tain returns by investing in riskier parts

of the infrastructure universe. Investment

manager skill sets and deal flow may be

less established in some of these areas and

the resulting blended portfolio may dem-

onstrate different return characteristics

compared with a pure PPP/PFI portfolio.

FINE LINES OF DIFFERENTIATION

In a period of consistently strong perfor-

mance and plentiful supply of new assets,

investors did not need to distinguish

between companies in the peer group. In

the evolving tighter environment, differ-

ences between companies become much

more important. This has resulted in a

greater degree of focus on total expenses,

deal flow, corporate governance, foreign

currency exposure and portfolio risks.

Companies are gradually responding

to the greater degree of scrutiny of valua-

tion assumptions, including life-cycle costs,

construction asset premiums, discount rates

and cashflow timing assumptions. Investors

are challenging investment managers on

related-party fees, special purpose vehicle

(SPV) director fees and the terms of related-

party transactions.

In an asset class where it can takemany

years to see the performance differences

from investment decisions, investors are

having to base their assessments on man-

agers’ and companies’ approaches. Compa-

nies that wish to continue growing need to

be able todemonstrate that they can source

attractive deals andprovide sufficient trans-

parency around these transactions and the

existing portfolio.

n

Tom Skinner

is head of research at Dexion Capital,

the London-based boutique investment bank

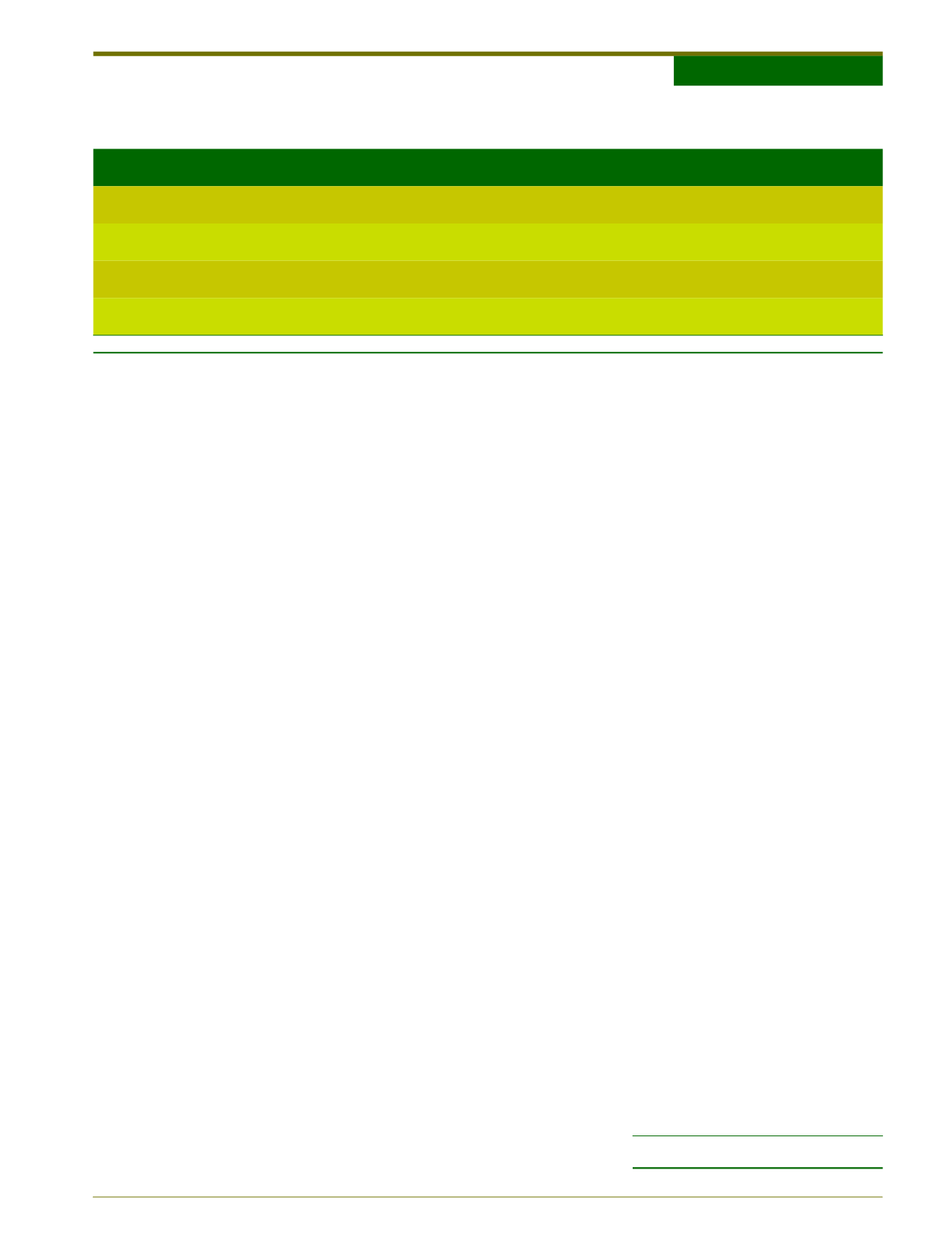

Name

Ticker Launch

Market

cap (£m)

Manager

Focus

Bilfinger Berger Global

Infrastructure

BBGI

21/11/2011 502

Internal

Minority UK exposure; currently highest construction exposure;

internally managed; youngest and smallest company

HICL Infrastructure

HICL 29/03/2006 1660

InfraRed

Largest and most established company; almost wholly third-party

acquisitions; highest UK exposure

International Public Partnerships INPP 08/11/2006 970

Amber

Infrastructure

Significant non-UK exposure; historically had meaningful construction

and non-traditional PPP exposure; highest fees

John Laing Infrastructure Fund JLIF 29/11/2010 889

John Laing Capital

Management

Pipeline agreement with John Laing; high UK exposure

THE LONDON LISTED PPP INFRASTRUCTURE EQUITY UNIVERSE

Source

: Dexion Capital